*Period ending 31st May, 2025, ** Rolling five year returns of all the Multicap PMSes reporting to PMS Bazaar *** For rolling five and three year periods from inception till date **** Five year Period ***** Three year period

In May 2025, Indian equity markets continued their upward momentum, driven by strong foreign portfolio investor (FPI) inflows and a broad-based risk-on sentiment. Defence and micro-cap stocks led the rally, with telecom, services, and capital goods sectors attracting substantial foreign interest, while traditional sectors like banking and IT saw some outflows. The month also witnessed record block deals and the highest FPI inflows of the year, indicating renewed global confidence. While equity mutual fund inflows dipped to a 13-month low, SIPs remained robust, hitting a new high. Macroeconomic tailwinds such as easing global inflation, a softer dollar, and expectations of rate cuts further supported sentiment. Despite the strong gains, elevated valuations—particularly in the small and mid-cap space—combined with rising geopolitical risks, suggest that caution may be warranted in the near term.

In May, the benchmark S&P BSE 500 TRI rose by 3.5%. Against that, Sameeksha PMS (Portfolio Management Service = Separately Managed Accounts) was up by 4.7% (net of all fees and expenses), indicating an outperformance of 1.2%; while having cash levels of 10% at start of the month and 5% at the end of the month.

As our PMS has completed fifty-one months of our five-year journey, we are taking this opportunity to reflect on our performance over the years through an insightful exercise—analyzing average five-year and three-year rolling returns across different time frames. What stands out the most is the consistency of alpha generation across various lookback periods. This stability indicates that the portfolio’s performance is not reliant on isolated stock picks or favorable market timing. Rather, it reflects a disciplined and repeatable investment process. The rolling return analysis reinforces that the outcomes are not driven by temporary market conditions, but are the result of a reliable, long-term approach to investing. We discuss the data in more detail later in this letter.

This consistent performance is further validated when benchmarked against the broader industry. When compared with the entire Multicap PMS universe reporting to PMS Bazaar, our strategy has consistently ranked in the top decile for five-year returns over fifty consecutive months.

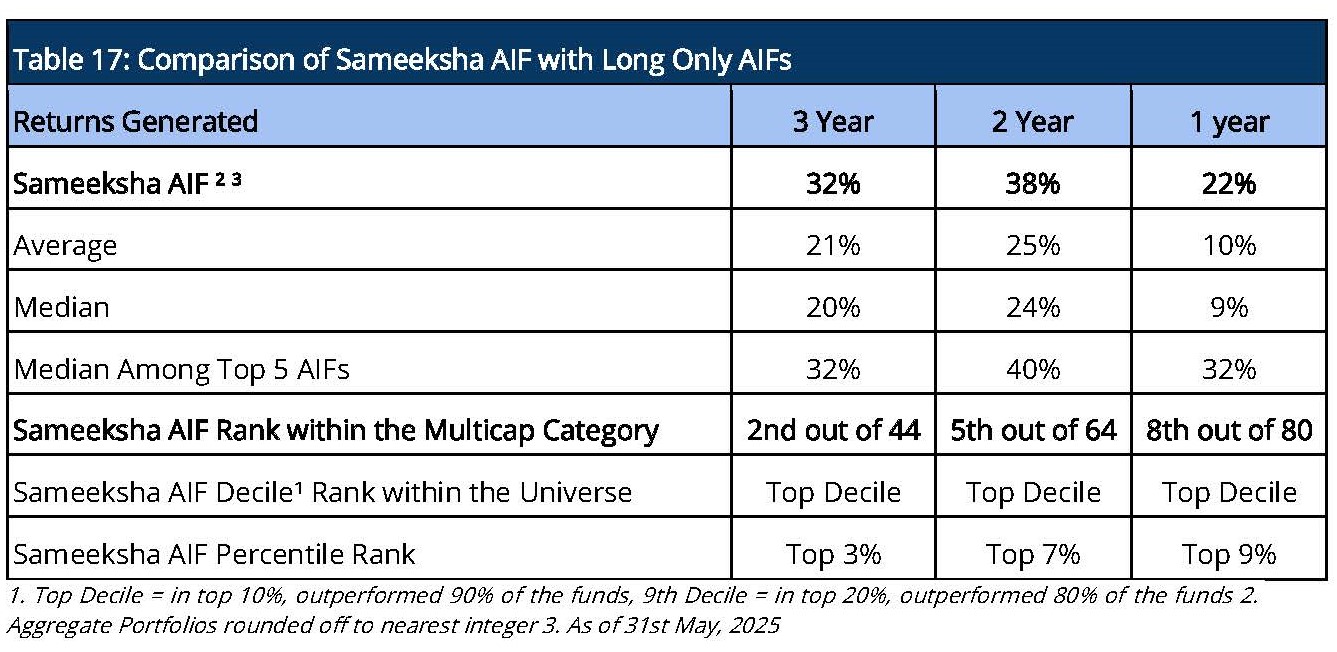

Sameeksha domestic AIF (Alternative Investment Fund = “Hedge Fund”) also continues to deliver top notch performance having recently completed three years of operating history. This AIF ranks right up at number two out of forty-four AIFs reporting their performance to PMS Bazaar. Our AIF was up by 5% (post fees and expenses), indicating an outperformance of 1.5% over the benchmark. Positive contributions came from FMCG, IT and Finance leading the Contribution at 1.61%. However, this was partly offset by negative contributions from the Banks, Crude Oil, and Telecom sectors. We compare our performance with some of the highly recommended mutual funds. We have compared returns, Sharpe Ratio as well as upside and downside capture ratios.

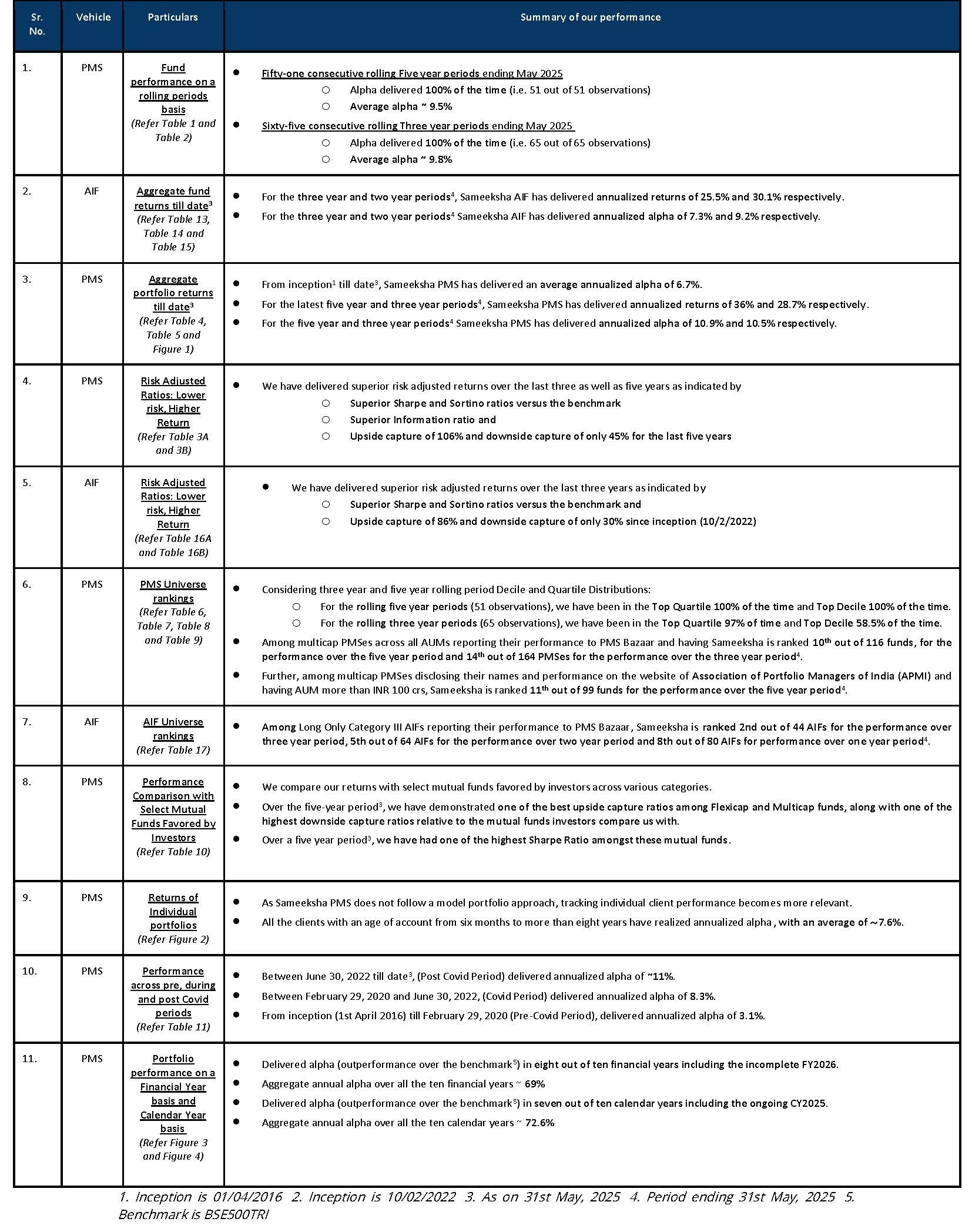

We summarize key aspects of our performance as follows:

PMS Performance and other details

Three important things must always be kept in mind when looking at performance data. First, for funds such as ours that do not follow model portfolio strategy, the performance of individual clients for different duration is important to look at. Second, some PMSes may be charging fees outside the PMS and hence after fees, performance data may not be comparable to ours. Third, it is important to look at not only portfolio returns but also risk adjusted ratios. We provide data to address all three points later in this note.

Aggregate Portfolio Performance and ranking on a rolling periods basis

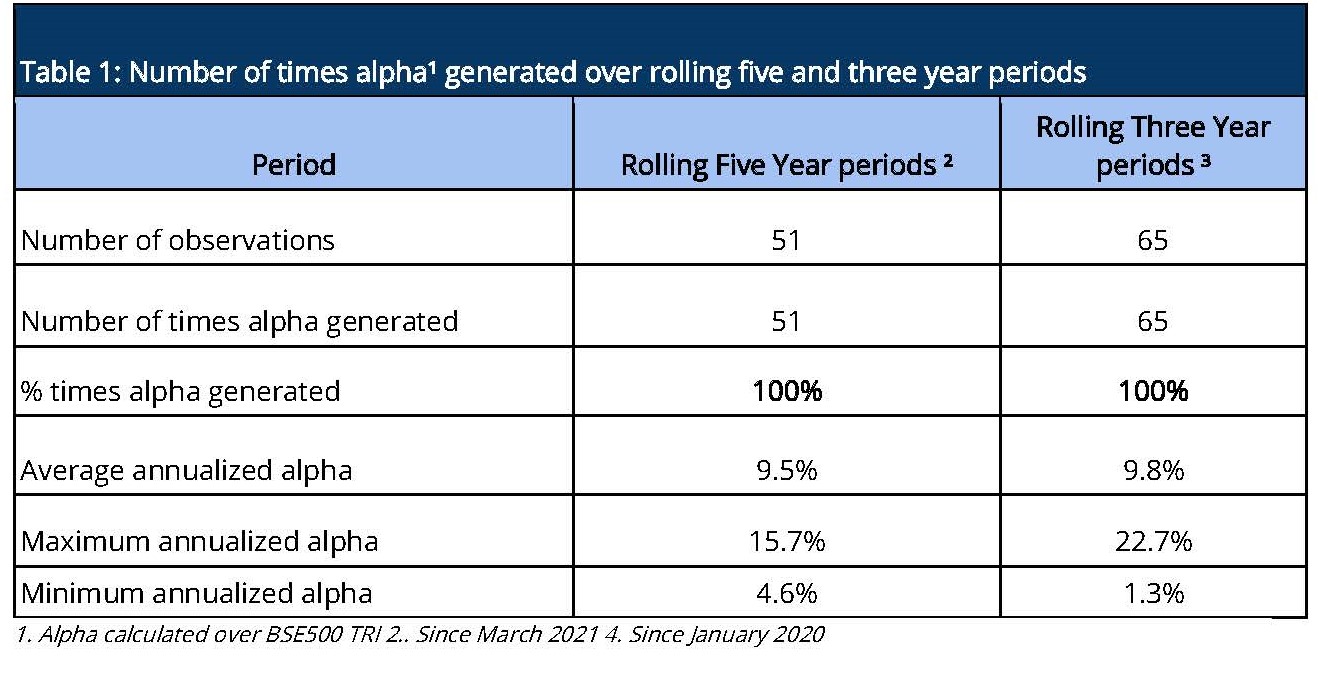

Rolling returns are a more useful indicator of consistency in performance versus single period returns. For the rolling five year periods applicable from March 2021 till date, Sameeksha PMS has delivered aggregate annualized alpha 100% of the time (51 out of 51 observations), ranging from ~5% to ~16%. For the rolling three year periods applicable from January 2020 till date, Sameeksha PMS has delivered aggregate annualized alpha 100% of the time (65 out of 65 observations) ranging from ~1% to ~23%. (Table 1). For both rolling five and three year periods covered in Table 1, alpha has averaged around 9.5% and 10% respectively.

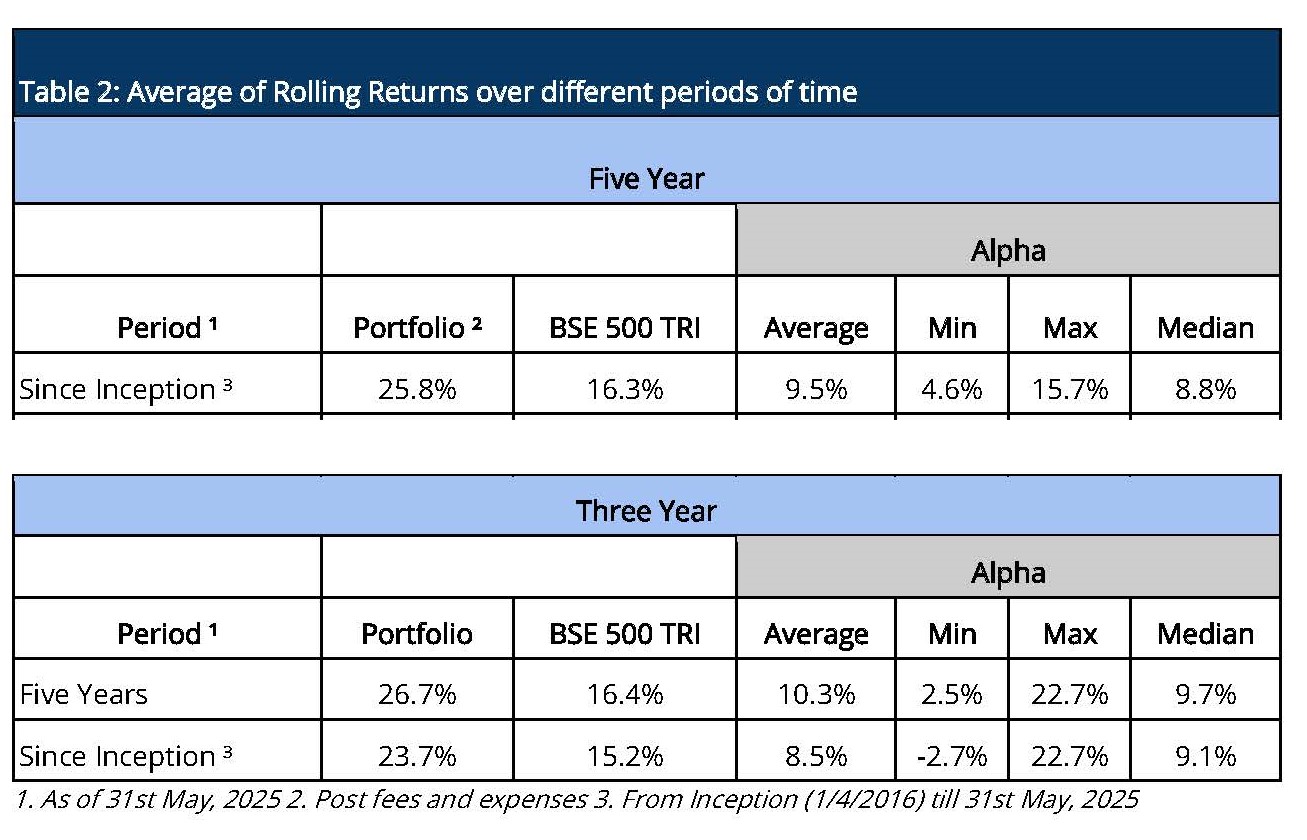

To analyse the rolling five year and three year returns, we did an insightful exercise, analyzing average five-year and three-year rolling returns across different time frames.

The table below (Table 2) presents the Sameeksha PMS’s portfolio performance using rolling five-year and three-year returns, a method that evaluates returns over overlapping periods ending on each date within a given time range . By averaging these rolling returns over different lookback periods, we gain a deeper understanding of how consistently the portfolio has delivered value over time, compared to the BSE 500 TRI benchmark.

The results reveal a strong and persistent pattern of outperformance. Across all measured periods, average three-year or five-year rolling returns have consistently outpaced the benchmark. What stands out in particular is the stability of alpha across different lookback periods. This consistency suggests that the portfolio’s success is not driven by isolated bets or favorable market timing, but rather by a disciplined and repeatable process. The rolling return framework helps illustrate that this performance is not a result of temporary market positioning, but instead reflects a reliable, long-term approach to investing.

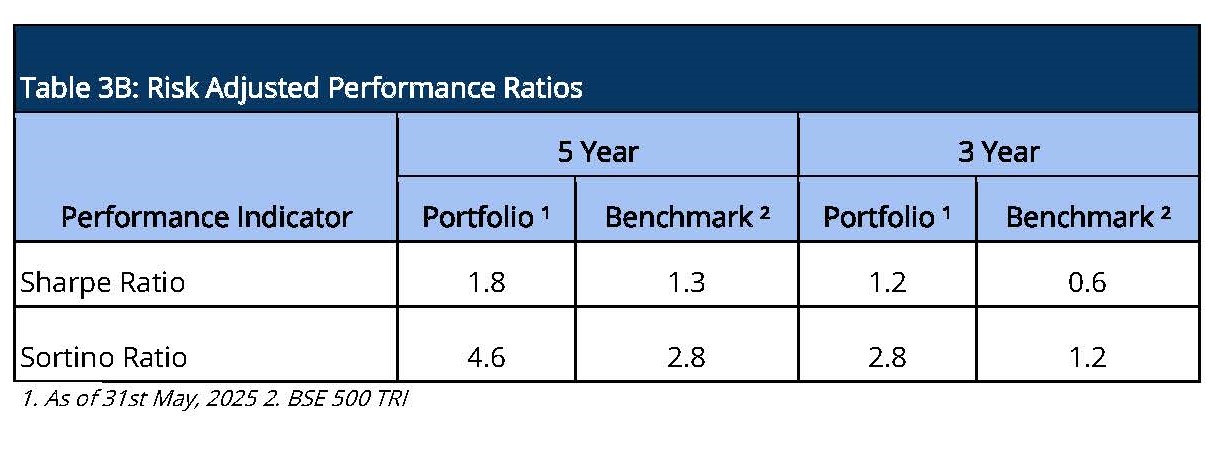

Risk Adjusted Ratios: Not all returns are the same, Higher Returns at lower Risk

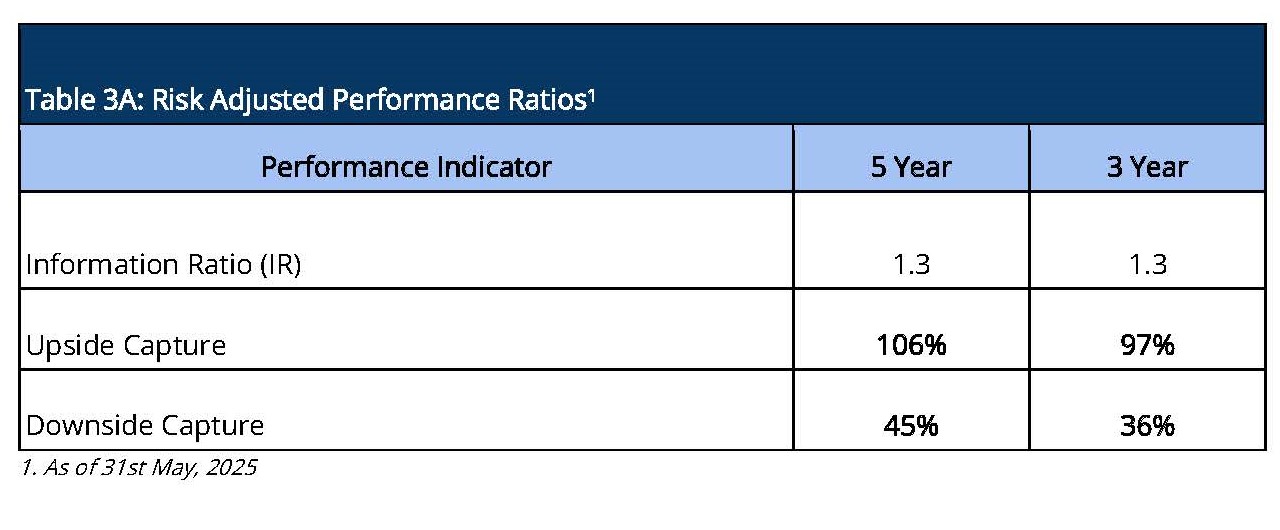

When compared on a risk adjusted basis, our PMS has shown an even stronger performance. The Information Ratio (IR) measures the excess return of a portfolio over a benchmark per unit of active risk. A higher Information Ratio suggests better risk-adjusted performance. The higher five year IR indicates better performance over the longer period in comparison to the IR in the three year period.

Moreover, Upside Capture measures how well a fund performs as compared to a benchmark when the benchmark has positive returns. A higher upside capture ratio (>100%) indicates that the fund captures more of the benchmark’s positive movements. Whereas, Downside Capture measures how well a fund performs compared to a benchmark when the benchmark has negative returns. A lower downside capture ratio (<100%) indicates that the fund preserves capital better during market downturns. (Table 3A).

Furthermore, other risk-adjusted returns – Sharpe ratio is also significantly higher. The Sortino ratio measures the risk-adjusted return of an investment, focusing only on the downside risk. A higher Sortino ratio indicates better risk-adjusted returns, particularly with respect to downside risk. (Table 3B).

Aggregate Portfolio Returns over various time periods

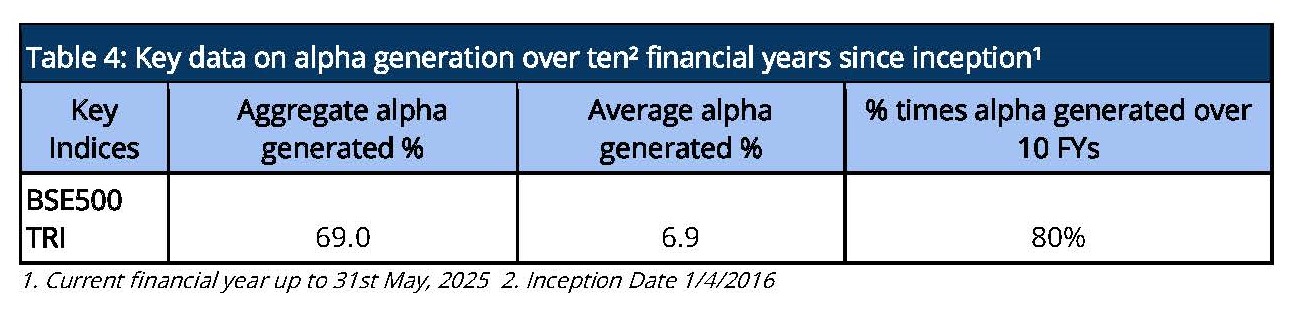

Sameeksha PMS has delivered a substantial aggregate annual alpha of 69% over BSE500 TRI over the ten financial years (including the current incomplete financial year) implying an average alpha of 6.9% since inception (Table 4).

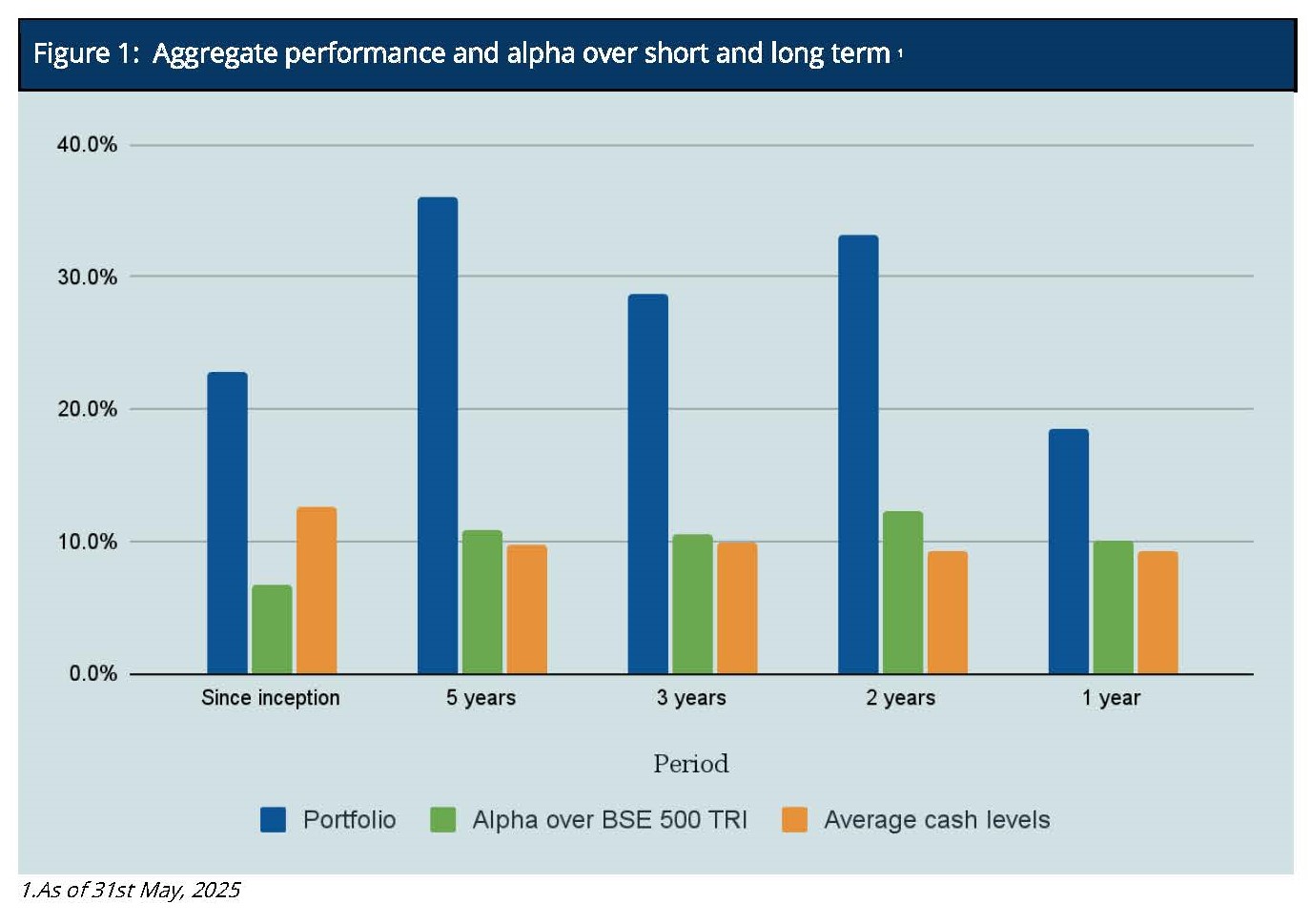

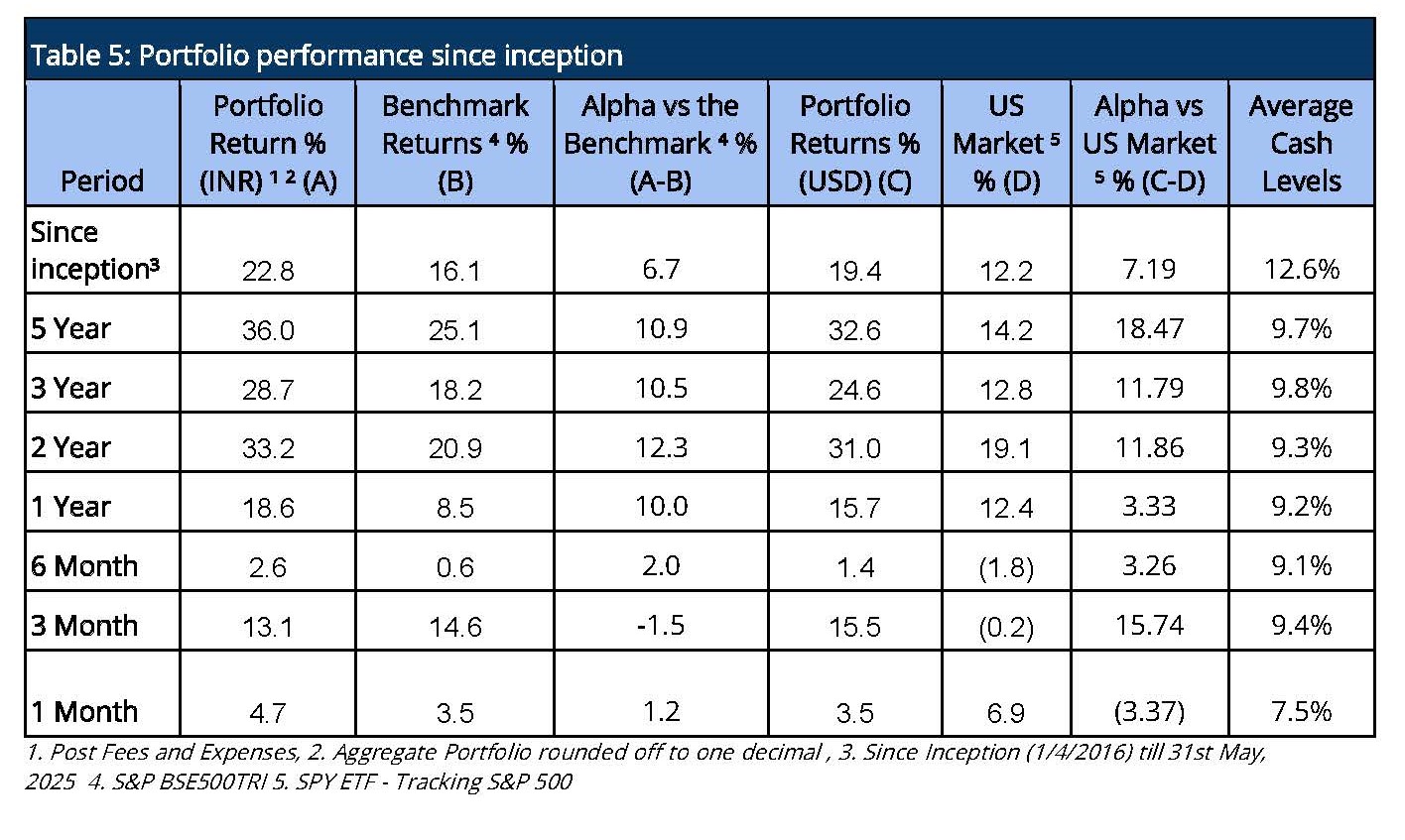

It is important to note that we have maintained relatively higher levels of cash (12.6% on average over the entire period since inception) from time to time over the duration of managing the portfolio. Notwithstanding the same, from inception, over five years and over three years respectively, we have generated returns of 22.8%, 36% and 28.7% in INR terms and 19.4%, 32.6% and 24.6% in USD terms thus generating substantial alpha over the Indian benchmark BSE500 TRI. Also, we have delivered strong returns relative to benchmark across various key time periods (Figure 1 and Table 5).

Performance within the PMS Universe

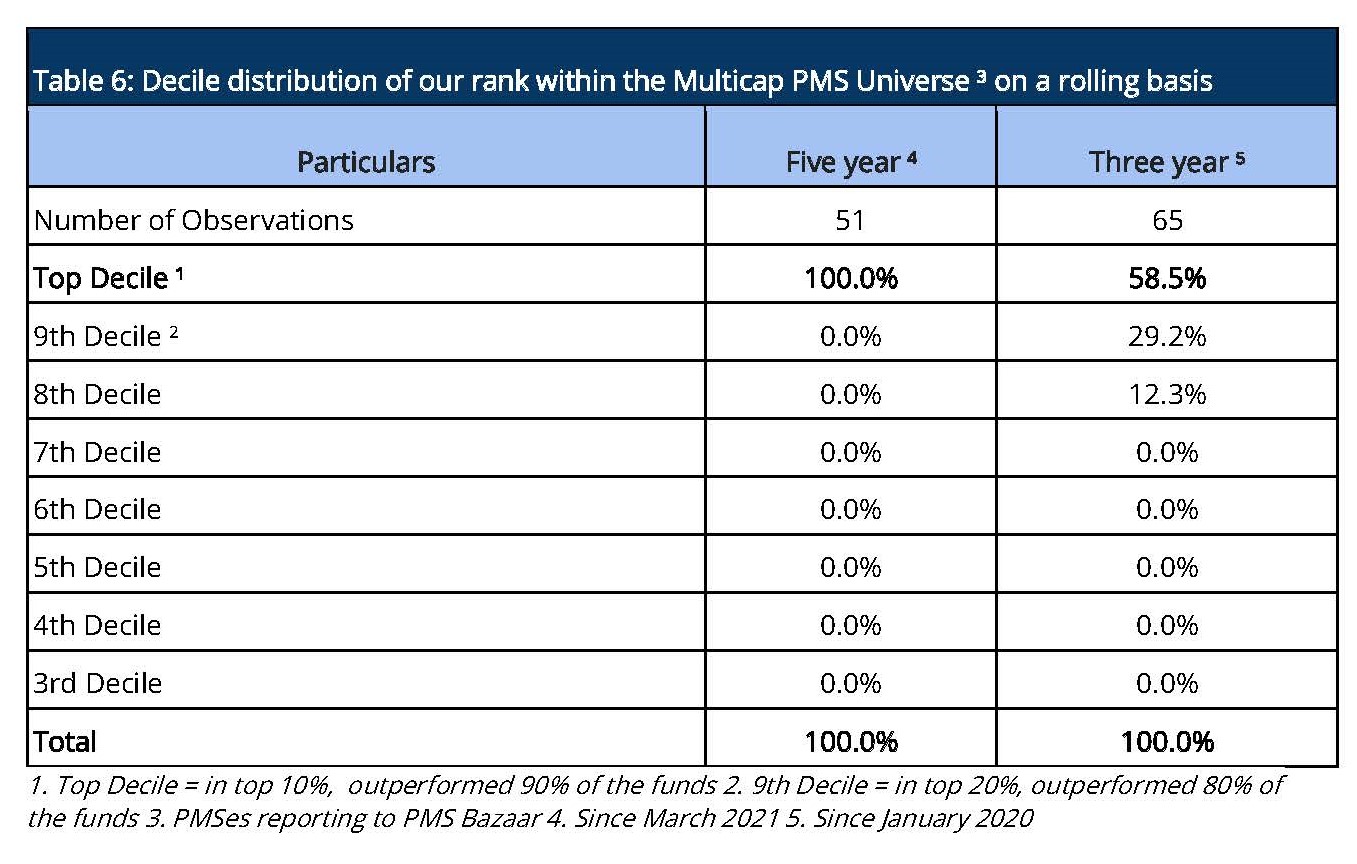

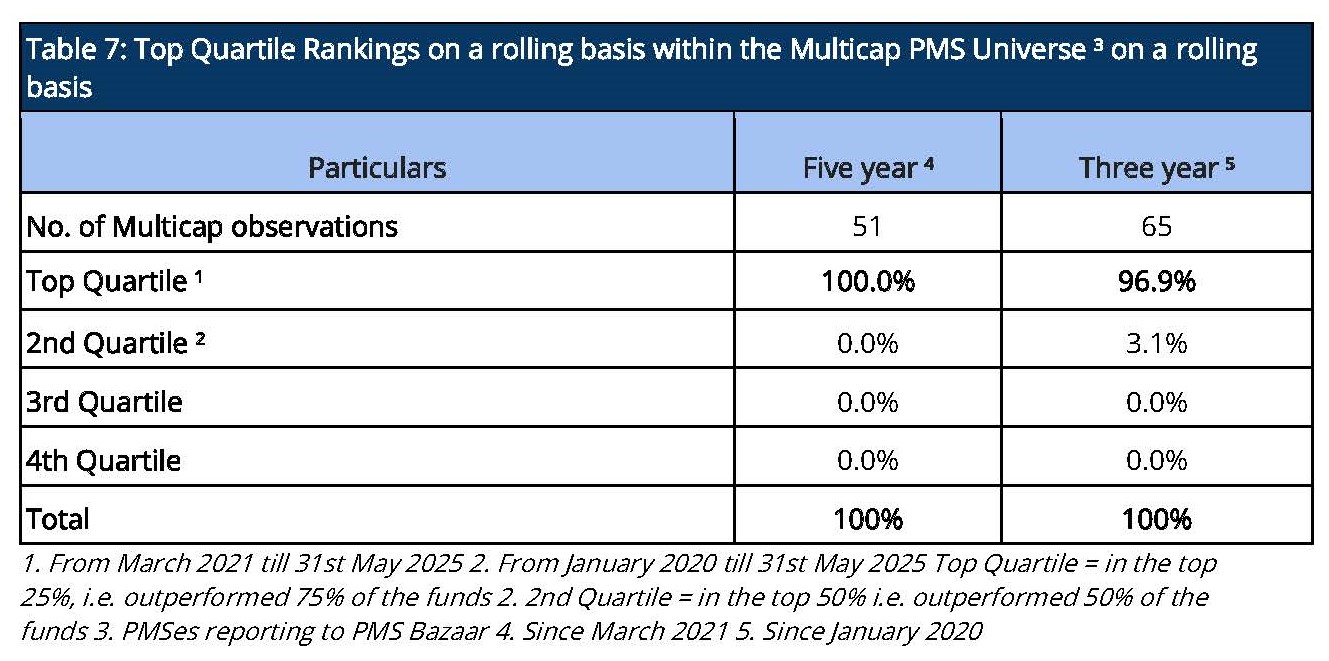

We continue to maintain our top rankings both within the multicap PMS universe as well as the entire PMS universe for key periods of three and five years. The multicap PMS universe rankings are more relevant to us since we follow the multicap strategy.

For rolling three year periods applicable since January 2020, we have been ranked among the multicap universe in the Top Decile 58.5% of the time (38 out of 65 observations) and in the Top Quartile 97% of the time (63 out of 65 observations). For rolling five-year periods applicable to our entire operating history, we have been ranked among the multicap universe in the Top Quartile 100% (51 out of 51 observations) and Top Decile 100% of the time (51 out of 51 observations). (Tables 6 and 7)

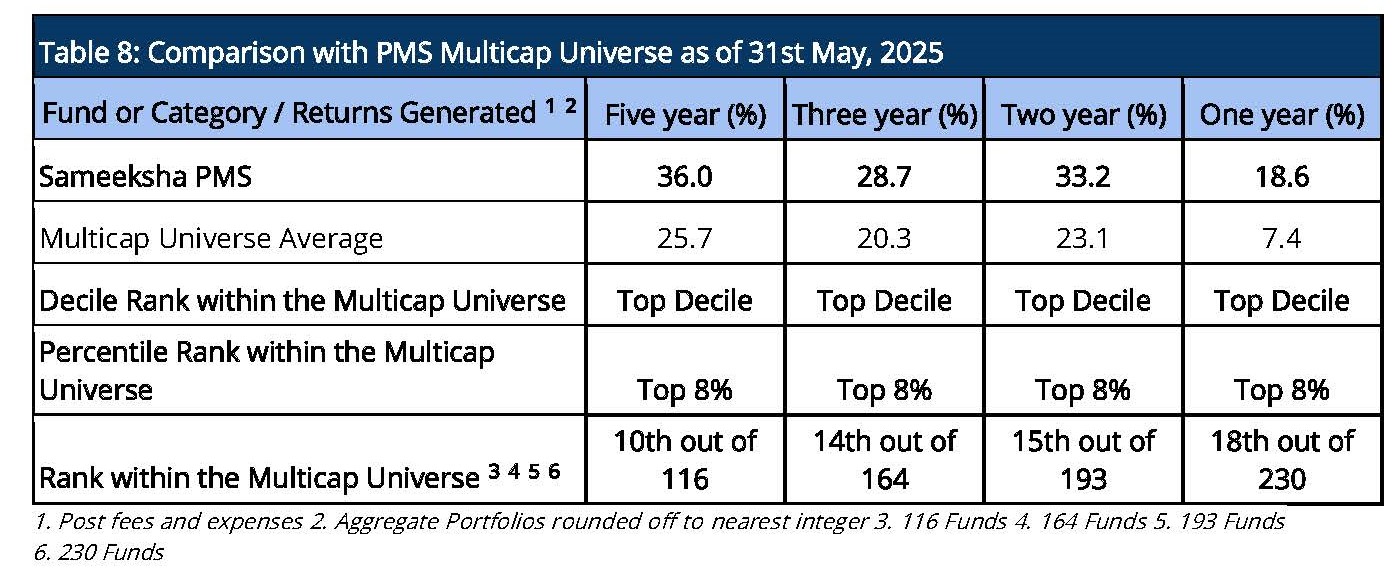

We present our rankings among those multicap PMSes across all AUM sizes. Within this universe, we are 10th out of 116 PMSes for the five year period and 14th out of 164 PMSes for three year period, highlighting our superior performance over the long term periods (Table 8). Among the multicap universe across all AUM sizes, we are consistently ranked in the Top Decile for the five year period for 51 out of 51 observations reflecting well on the consistency of our performance.

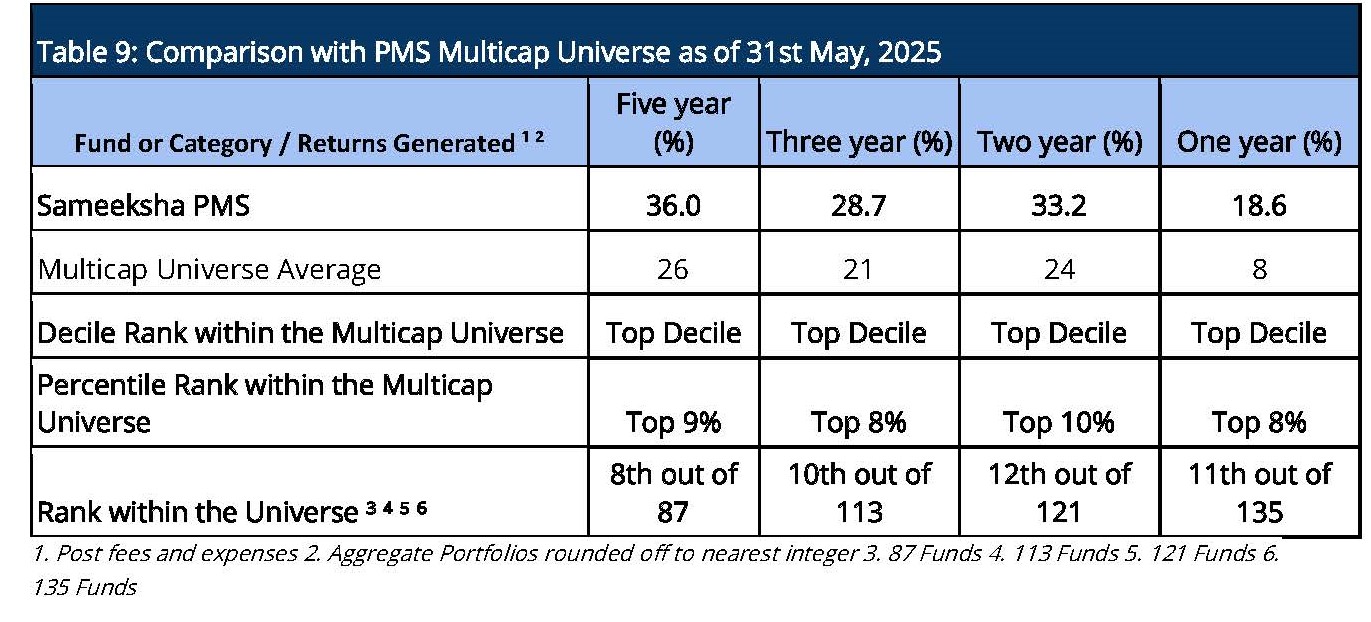

We also want to share our ranking among all Multicap PMSes having an AUM of more than or equal to INR 100 crs. Within this universe, we are ranked 8th out of 87 PMSes for the five-year period and 10th out of 113 PMSes for the three-year period (Table 9).

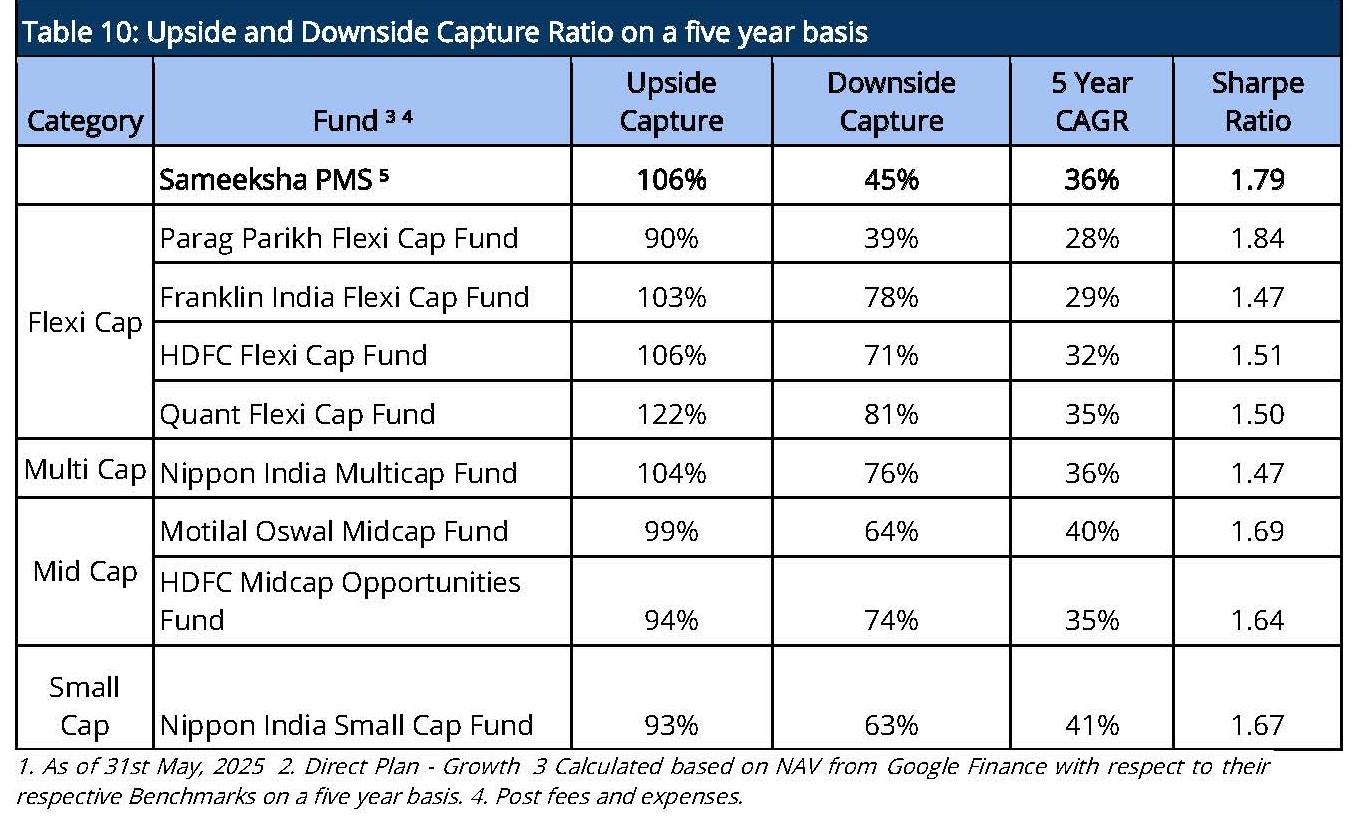

Performance Comparison with Select Mutual Funds Favored by Investors

We compare our returns with a group of mutual funds favored by investors across various categories. This ensures that our performance assessment is both relevant and insightful, focusing on funds that align with investor preferences. We have achieved one of the lowest downside capture ratios compared to the mutual funds we analyze, reflecting our strong emphasis on risk management and minimizing losses during market downturns. Over a five-year period, we have delivered superior returns compared to these mutual funds, both in terms of CAGR as well as risk-adjusted returns, showcasing our ability to generate consistent and sustainable performance (Table 10)

Returns of Individual Portfolios

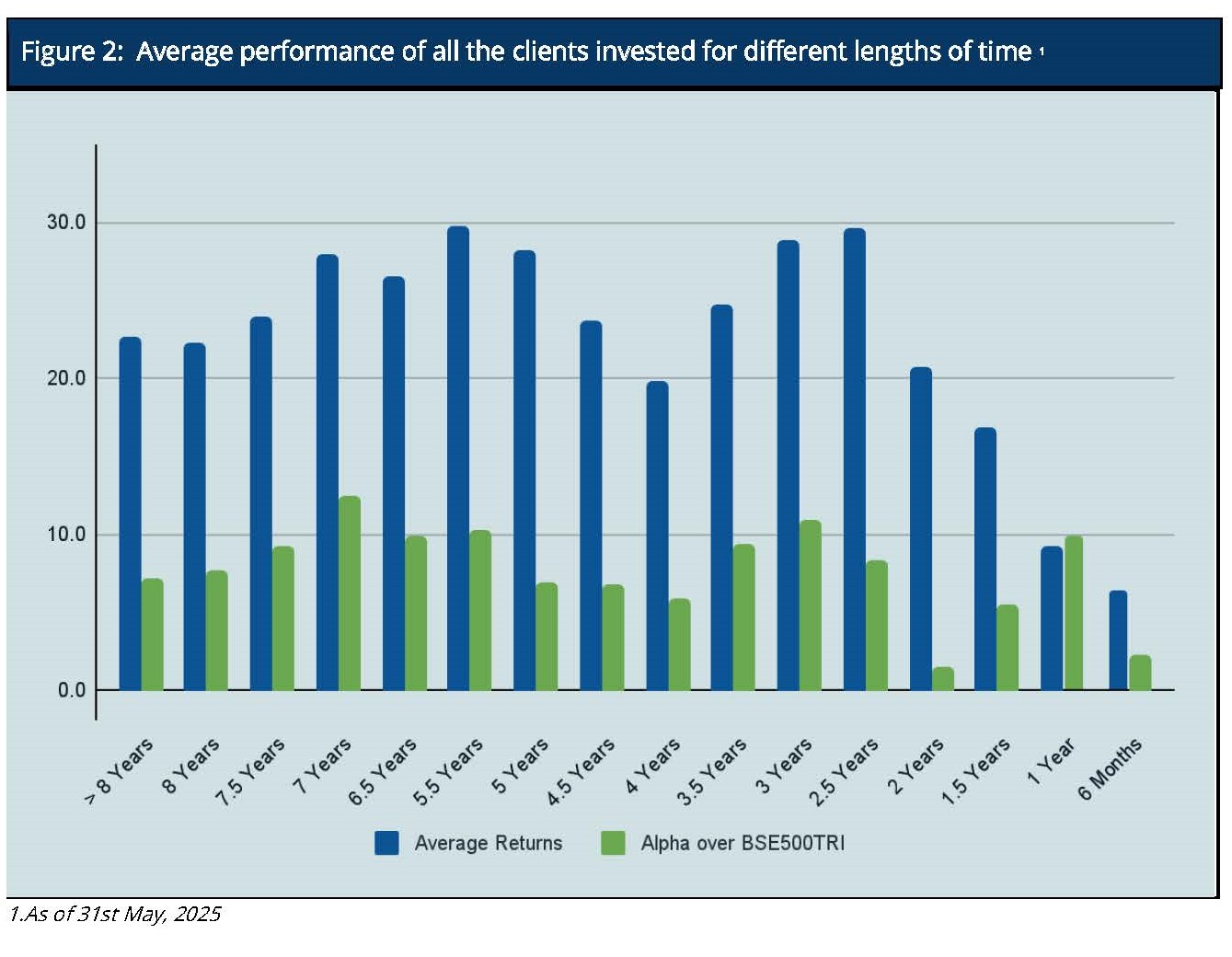

Because we don’t follow model portfolio strategy, the performance of individual clients is far more important than overall portfolio aggregate returns (Figure 2). For investors who are with us for five years and more, Sameeksha PMS has returned a very substantial alpha with an average annualized alpha of approx. 8.8% for the five year period ending 31st May, 2025. Similarly, for investors who are with us for three years or more, Sameeksha PMS has returned substantial alpha with an average annualized alpha of approx. 9.7% for the three year period ending 31st May, 2025. The Figure below shows the average annualized returns and alpha over different periods of time of all the clients as on 31st May, 2025.

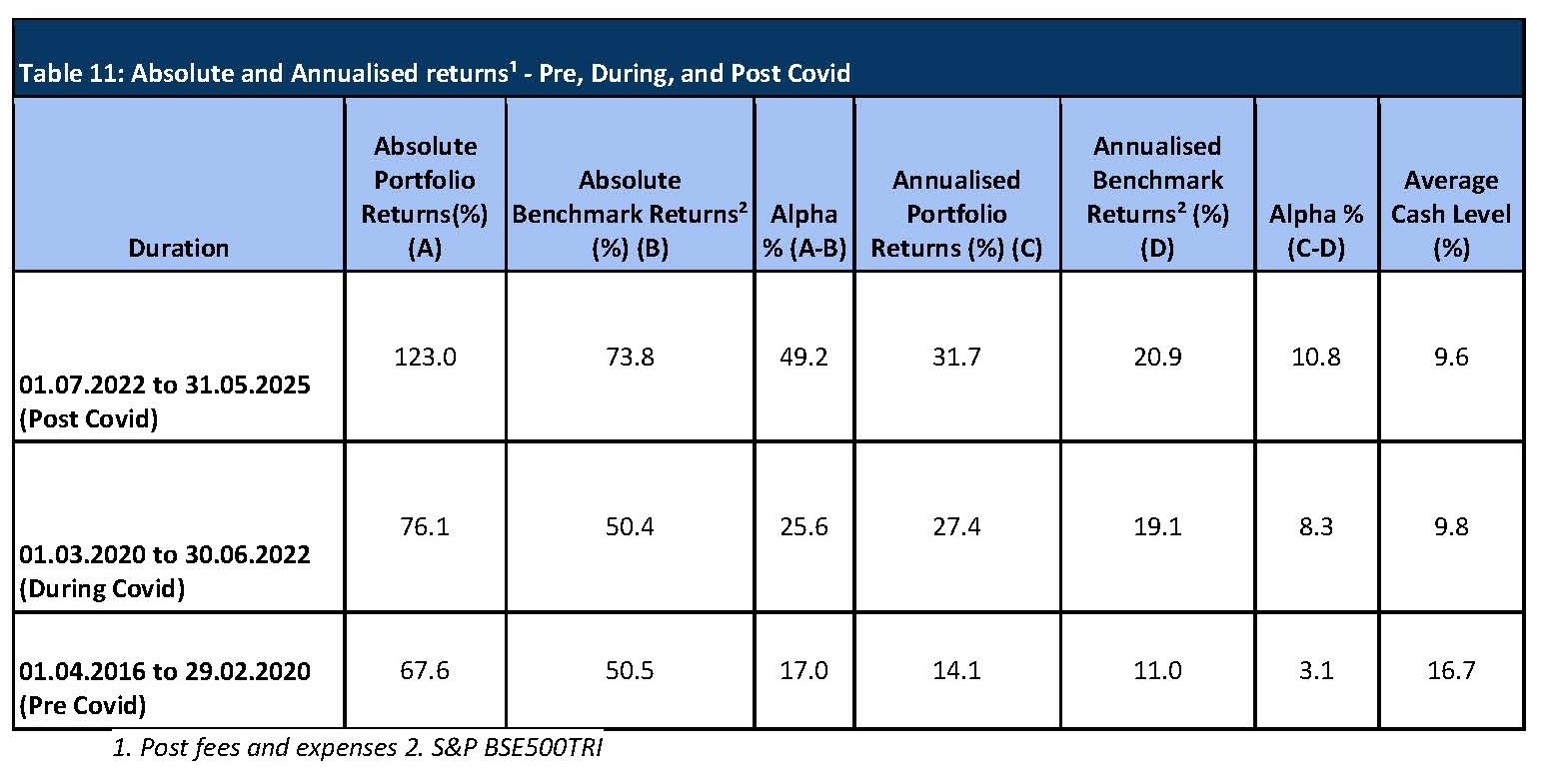

Performance Of PMS Over The Covid Timeline (Pre, During, And Post)

The Covid Pandemic induced significant volatility in the equity markets. Hence, it is useful to look at the performance across three time slices : Pre Covid, During Covid and Post Covid. Sameeksha PMS has outperformed the benchmark across all of these three time periods with meaningful alpha (Table 11). This consistency of performance may be an important factor in comparing us with the other funds.

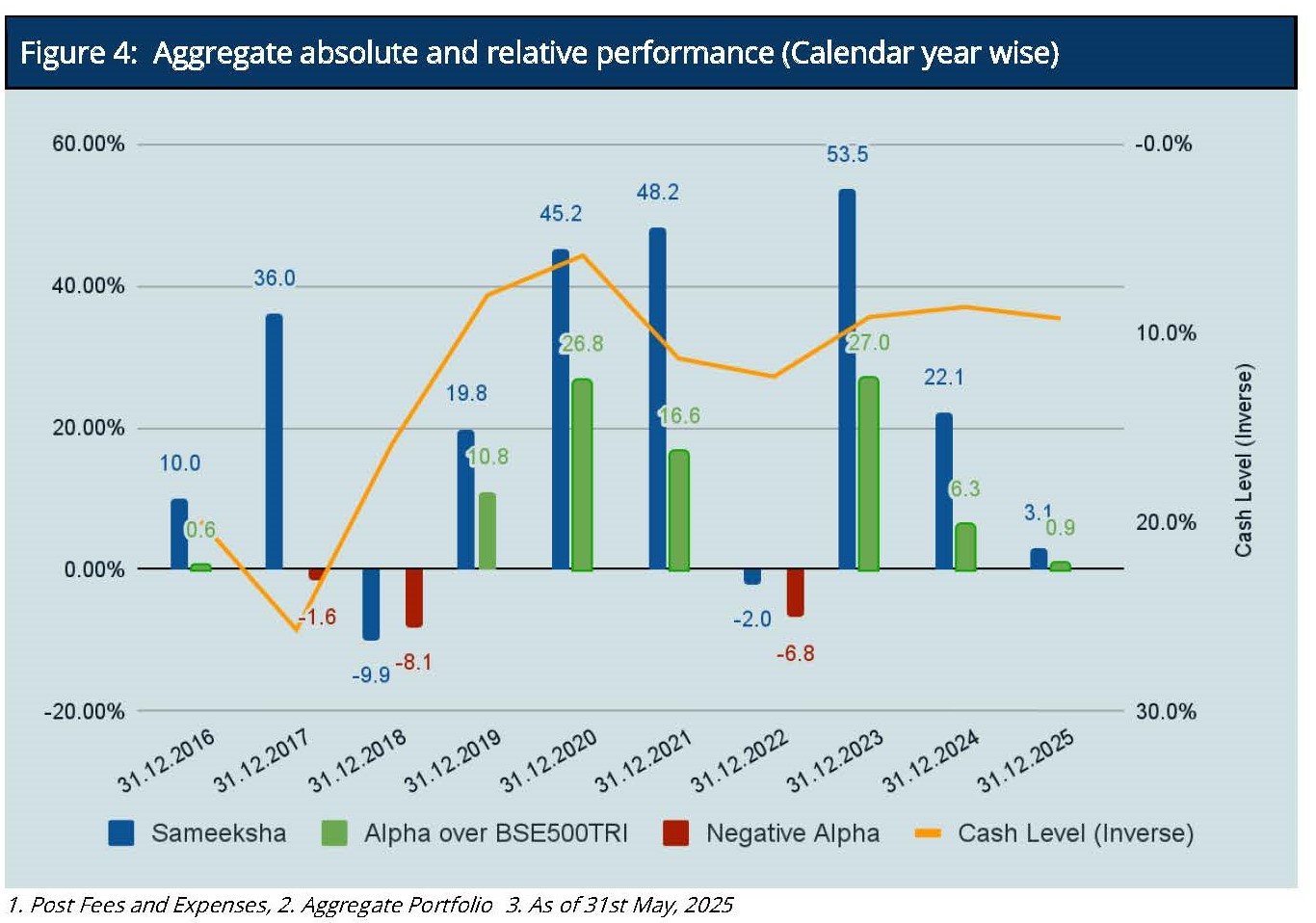

Aggregate Portfolio Performance on a financial year and calendar year basis

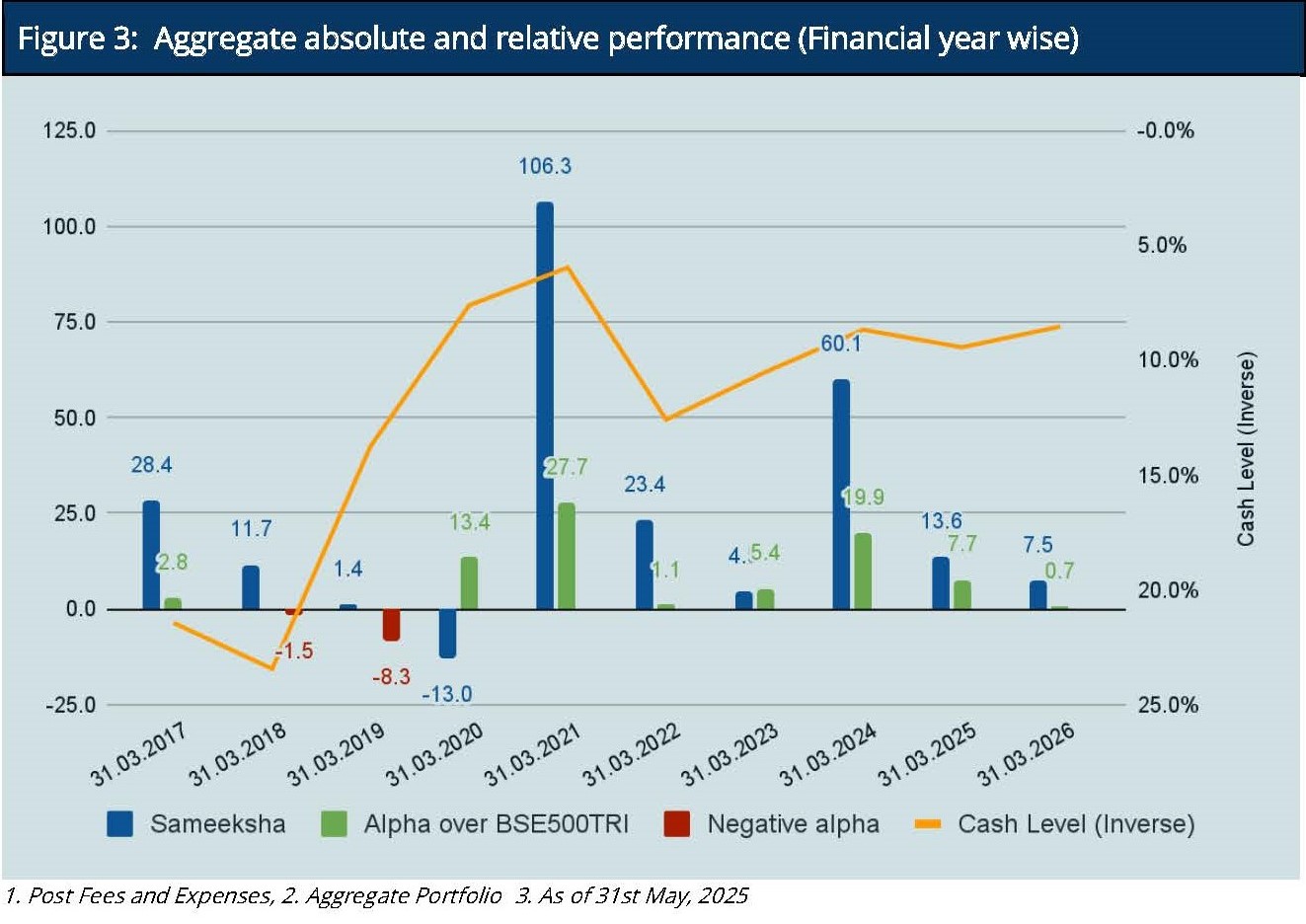

For the month of May, Sameeksha PMS has outperformed the benchmark BSE 500 TRI by 1.2%. For Financial Year 2025-26, we have outperformed BSE500 TRI by 0.7%. Looking at our performance over the financial years (Figure 3), we have outperformed our benchmark in eight out of ten financial years. Key however is that the sum of outperformance of 78.8% in those eight years far exceeds the sum of underperformance of 9.8% in the remaining two years. We have successfully outperformed in the previous financial year, marking six consecutive years of generating alpha.

For the Calendar Year 2025, we have marginally outperformed the benchmark BSE500 TRI by 0.9%. Looking at our performance over calendar years (Figure 4), we have outperformed the benchmark in seven out of ten calendar years and the sum of outperformance of 89.1% in seven years far exceeds the sum of underperformance of 16.5% in the remaining three years.

It is important to note that we delivered this alpha despite maintaining an average cash level of 12.6% across the ten financial years.

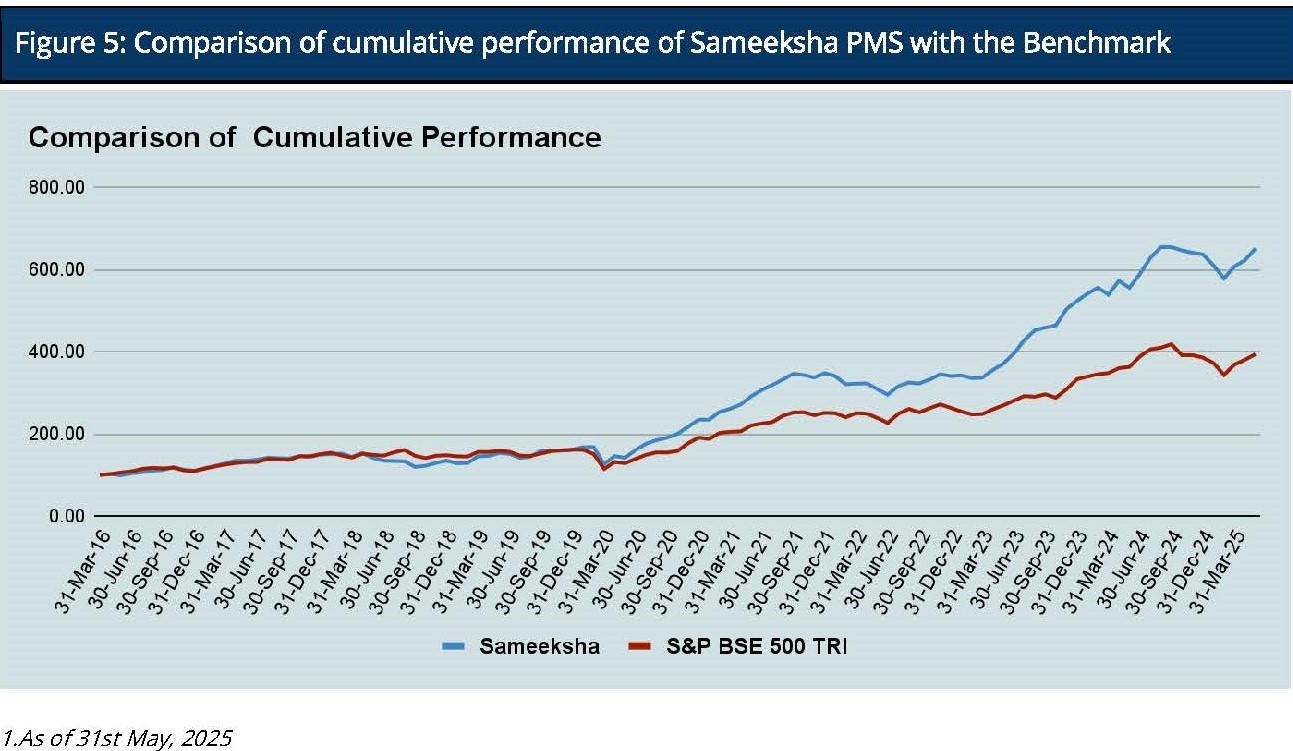

Cumulative Performance versus the benchmark

Sameeksha PMS’s outperformance over its benchmark has continued to widen positively over the years. An investment of Rs. 100 with us since inception (April 2016) would have grown to Rs.650.5, far outpacing what one would have earned by investing in a fund that achieved benchmark returns (Figure 5).

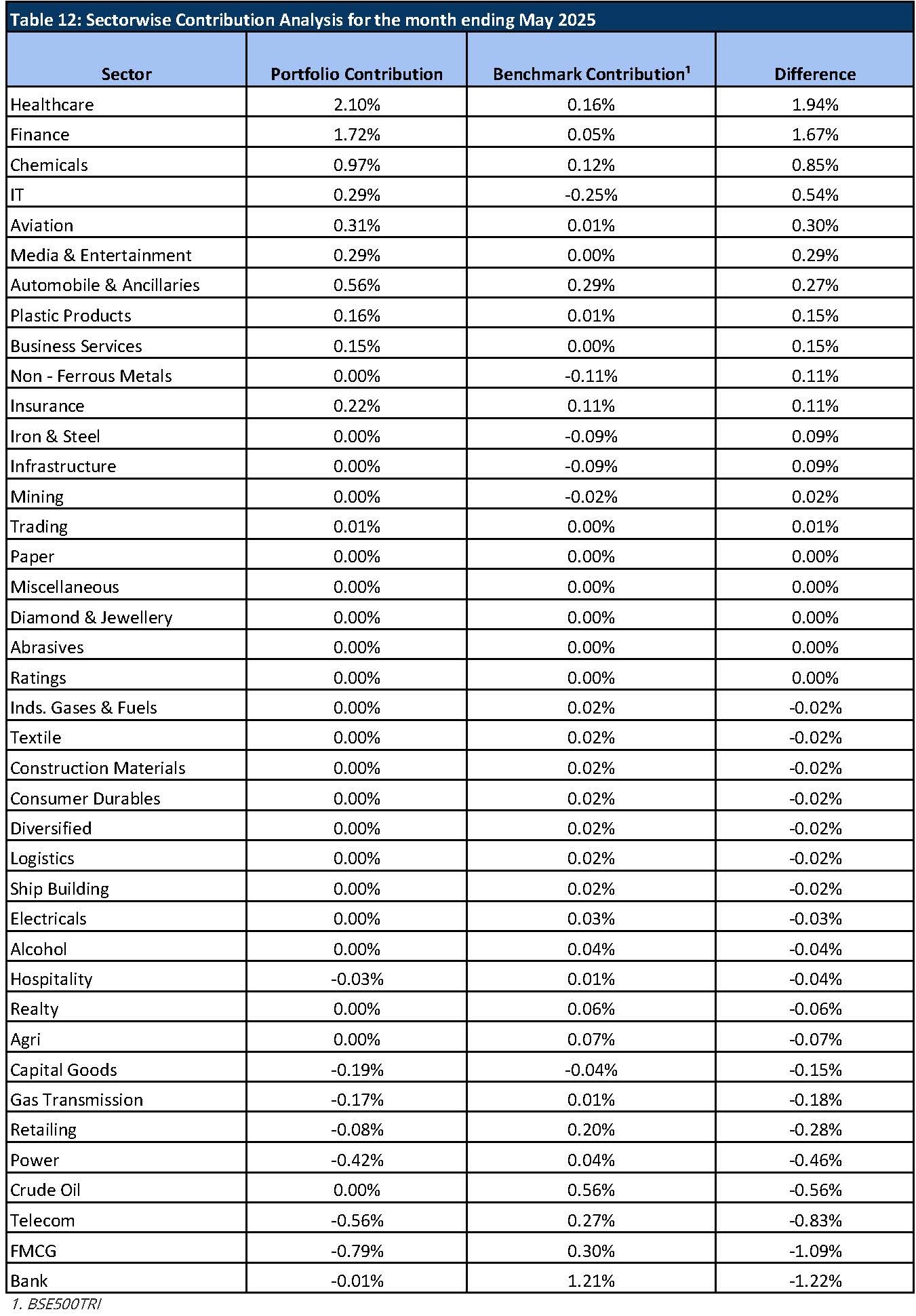

Analyzing the sector performance during the month

The contribution analysis of May 2025 reveals that the portfolio is performing well in sectors like Healthcare, Finance and Chemicals, which are significantly outperforming their benchmark counterparts. These sectors have provided positive contributions to the portfolio, with Healthcare leading at a 1.94% difference. On the other hand, Telecom, FMCG and Banks are notable underperformers, contributing negatively to the portfolio, with Banks underperforming by -1.22% relative to the benchmark.

Below is the contribution analysis for the month of May 2025 (Table 12).

AIF Performance and other details

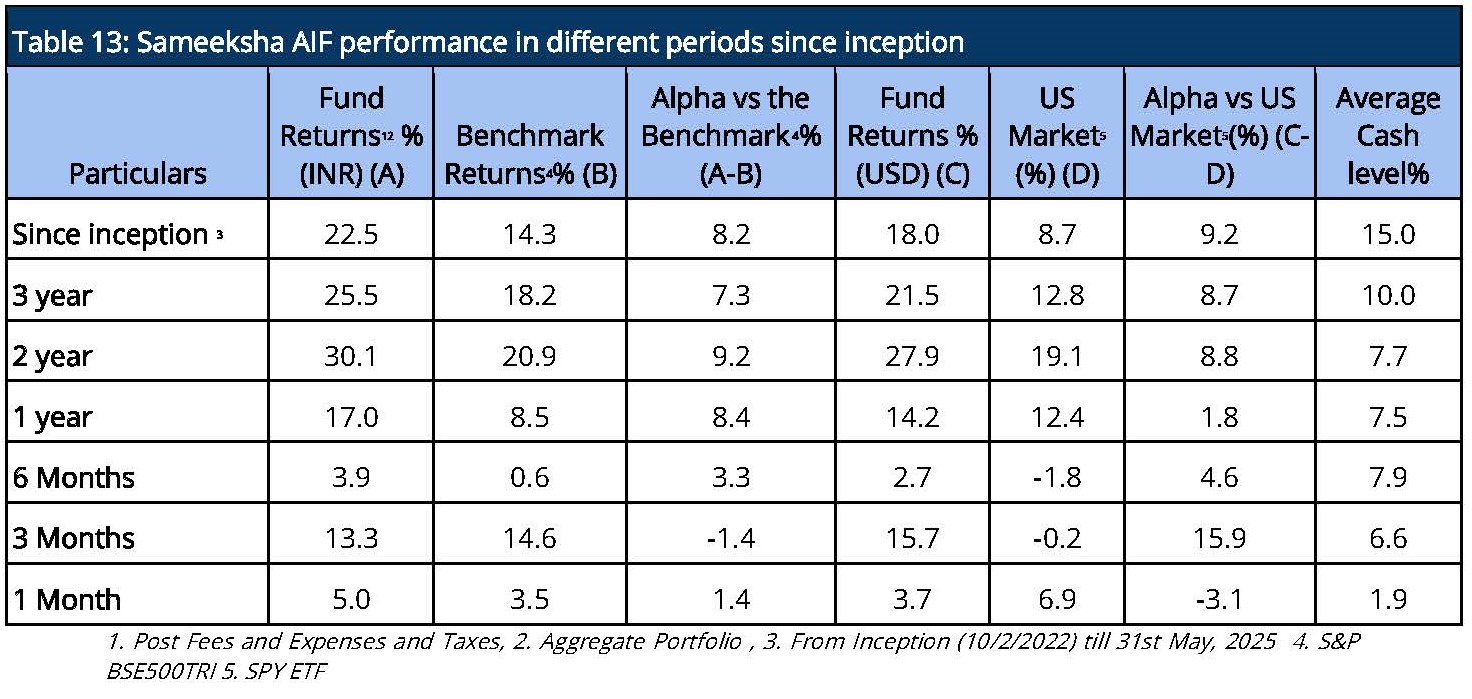

Aggregate Fund Returns over various time periods

Since inception, we have maintained relatively higher levels of cash (15% on average over the entire period from inception) from time to time over the duration of managing the fund. Notwithstanding the same, from inception, over three years and over two years, we have generated returns of 22.5%, 25.5% and 30.1% in INR terms and 18%, 21.5% and 27.9% in USD terms beating the benchmark BSE500 TRI returns and ETF tracking S&P 500 index, respectively after fees and taxes. (Table 13).

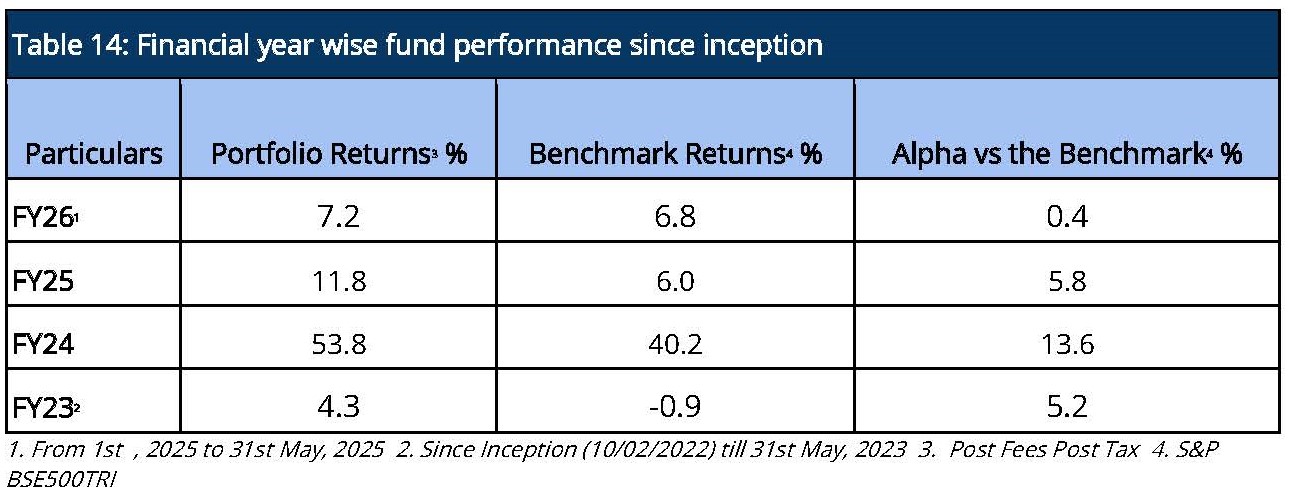

Aggregate Fund Performance on a financial year and calendar year basis

For the month of May, Sameeksha AIF has outperformed the benchmark BSE 500 TRI by generating 7.2% returns against the benchmark BSE500TRI returns of 6.8%. Looking at our performance over the financial years (Table 14), we have outperformed our benchmark in FY 2023, FY 2024 and FY 2025 and we will continue to outperform in the current incomplete FY 2026. For the Financial year 2026 till date, we have positioned ourselves by slightly outperforming the benchmark BSE500 TRI by 0.4%.

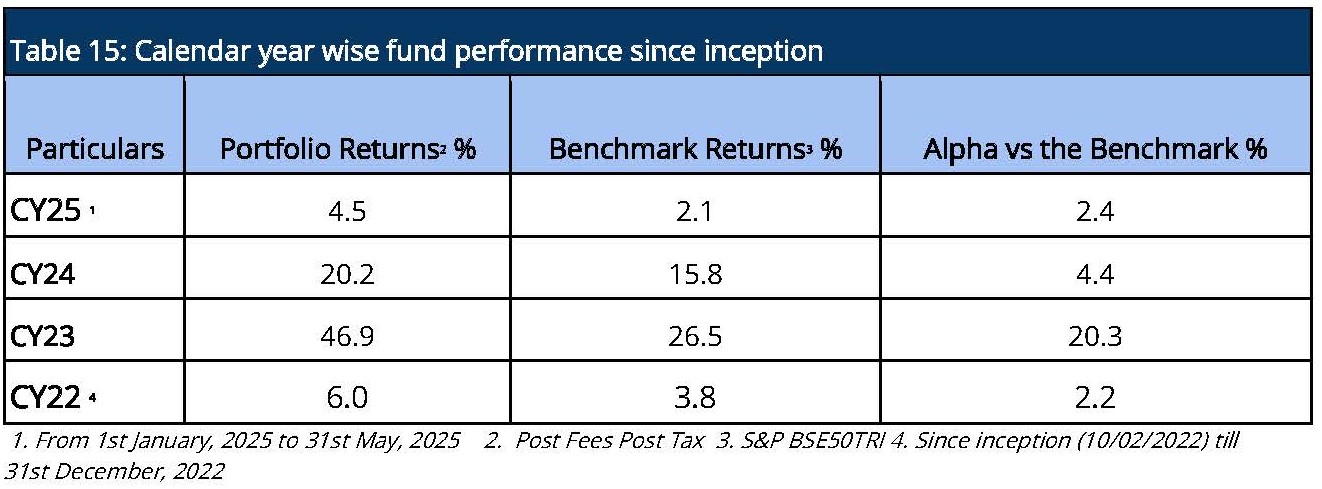

For the Calendar year 2025, we have outperformed the benchmark BSE 500 TRI by 2.4%. Despite being a new fund, we were still able to produce alpha for calendar years 2022, 2023 and 2024 and outperformed the benchmark BSE500 TRI by 2.2%, 20.3% and 4.4% respectively. (Table 15)

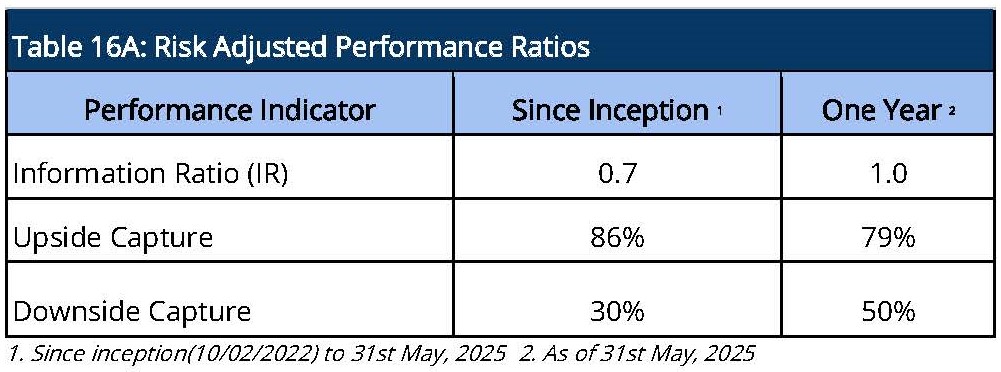

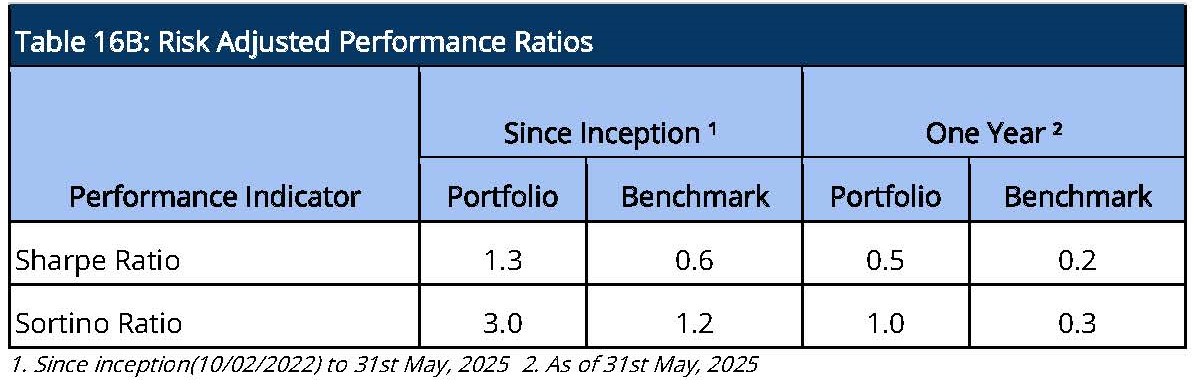

Risk Adjusted Ratios

When compared on a risk adjusted basis, our AIF has shown an even stronger performance. The Information Ratio (IR) measures the excess return of a portfolio over a benchmark per unit of active risk. A higher Information Ratio (IR) suggests better risk-adjusted performance.

Moreover, Upside Capture measures how well a fund performs as compared to a benchmark when the benchmark has positive returns. A higher upside capture ratio (> 100%) indicates that the fund captures more of the benchmark’s positive movements. Whereas, Downside Capture measures how well a fund performs compared to a benchmark when the benchmark has negative returns. A lower downside capture ratio (< 100%) indicates that the fund preserves capital better during market downturns. (Table 16A)

Furthermore, other risk-adjusted returns – Sharpe ratio is also significantly higher. The Sortino ratio measures the risk-adjusted return of an investment, focusing only on the downside risk. A higher Sortino ratio indicates better risk-adjusted returns, particularly with respect to downside risk. (Table 16B).

Performance within the AIF Universe

We present our rankings among Long Only Category III AIFs. For the period ending 31st May, 2025 , we are ranked 2nd out of 44 AIFs for the three year period, 5th out of 64 AIFs for the two year period, and 8th out of 80 AIFs for the one year period (Table 17). Sameeksha has been Top Decile consistently in the last three years. Because there is a lot of divergence in the way funds report their returns (post exp & tax; post exp, pre tax; gross returns; and post exp & tax pre perf. fees &) , we are doing comparison on a gross return basis to cover the entire applicable universe of funds.

Cumulative Performance versus the benchmark

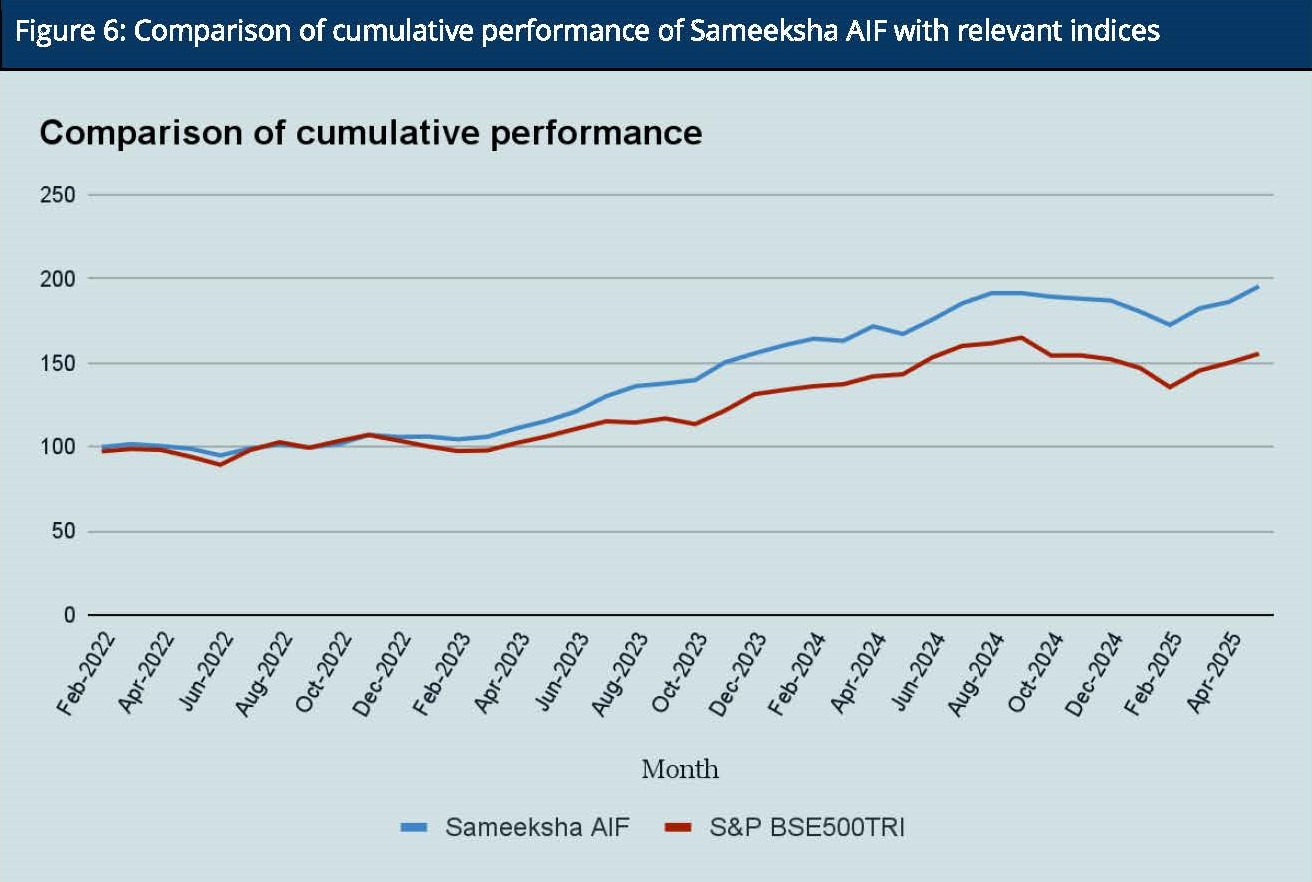

Sameeksha AIF’s outperformance over its benchmark has continued to widen positively since inception. An investment of Rs. 100 with us since inception (Feb 10,2022) would have grown to Rs. 195.5, far outpacing what one would have earned by investing in a fund that achieved benchmark returns (Figure 6).

Analyzing the sector performance during the month

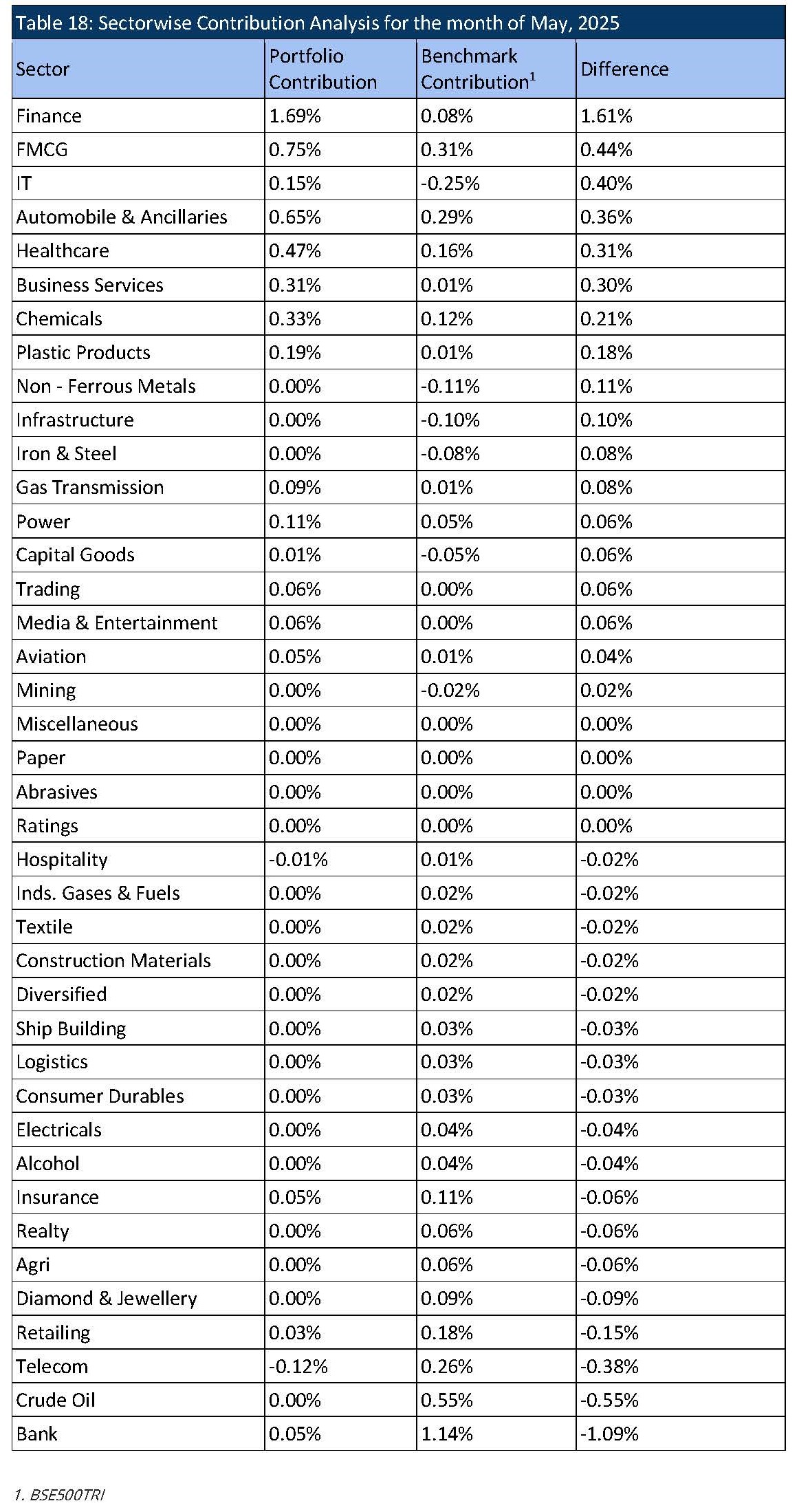

Sameeksha AIF outperformed the benchmark in May 2025, driven by significant overweight positions in Finance, FMCG, and IT—sectors that delivered strong results. Additional gains were supported by solid contributions from Healthcare, Automobiles & Ancillaries, and Business Services. Selective exposure to niche areas such as Non-Ferrous Metals and Aviation further added alpha. The portfolio maintained broad diversification, while notably underweight in sectors like Banking, Crude Oil, and Telecom helped mitigate downside risks and contributed to relative outperformance. (Table 18)

Disclaimer – The information contained in this update is provided by our fund accounting platform and is not audited. This document is for informational purposes only and is not intended for solicitation to residents of the United States or any other jurisdiction which would subject Sameeksha Capital or its affiliates to any registration requirement within such jurisdiction or country. It does not constitute an offer to buy or sell securities or financial instruments. Recipients are advised to conduct their own research and seek professional advice before making any investment decisions.