This month gave a ray of hope after a rather challenging 2022. While RBI has continued with its hawkish stance towards rate hikes, the inflation has cooled off marginally and the crude oil prices have come off as well. There was also a turnaround in the FPI sentiments where the FPIs became net buyers in July after being net sellers in the first six months of 2022. The benchmark BSE500 rallied significantly to return 9.76% in July 2022, up from -5.1% in June 2022. This month was a respite for us too since Sameeksha PMS gained on absolute terms by generating 7.05%. However, relatively, Sameeksha PMS underperformed the benchmark by 2.71%.

Among the multicap PMS universe tracked by PMS Bazaar, we are ranked 5th out of 59 multicap PMSes for the five year period ending July 2022,. For the three year period ending July 2022, we are ranked 8th out of 102 multicap PMSes reporting to PMS Bazaar.

As defined by our strategy, we have maintained relatively higher levels of cash (14% on average over the entire period from inception) from time to time over the duration of managing the portfolio. Notwithstanding the same, from inception as well as over five and three years respectively, we have generated returns of 19.9%, 17.4% and 30.8% beating the benchmark BSE500 TRI returns of 15.5%, 12.3% and 19.2% respectively

Portfolio Returns

For the month of July 2022, the broader markets ended on a strong note with the benchmark indices rallying significantly in this month. We had a relatively healthier month as compared to the last six months; however our performance this month i.e. 7.05% is still lower than the benchmark BSE500 TRI returns of 9.76%. While our returns are significant for longer periods, we are not happy with our performance over the last one year. Throwing light on our average performance, we have discussed our performance for the last financial year in our annual investor letter, including what did and did not work well for us, and our outlook on the Indian market.

As can be observed in Table 1, we have strongly outperformed our benchmark index across all the other relevant key periods –

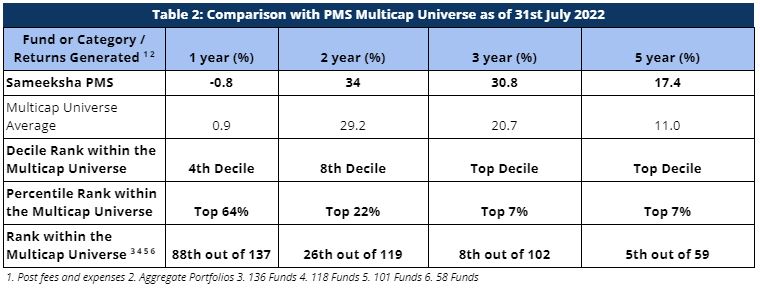

Performance within the PMS Universe

We continue to maintain our top rankings both within the multicap PMS universe as well as the entire PMS universe for key periods of three and five years. The multicap PMS universe rankings are more relevant to us since we follow multicap strategy.

For the three year period, we are ranked 8th out of 102 PMSes. Further, we are ranked 5th out of 59 funds for the five year period comparison within the Multicap universe – highlighting our superior performance over the long term (Table 2).

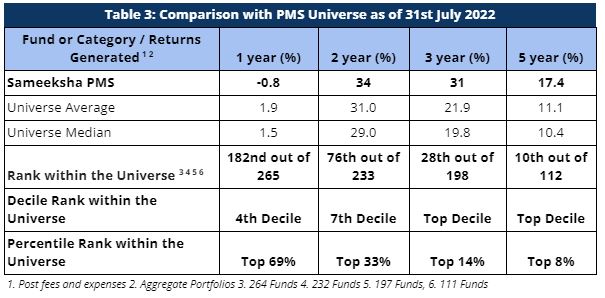

When compared with the entire PMS universe, we have maintained top rankings for longer key periods. We are ranked 28th out of 198 PMSes for the three year period and 10th out of 112 PMSes for the five year period (Table 3)

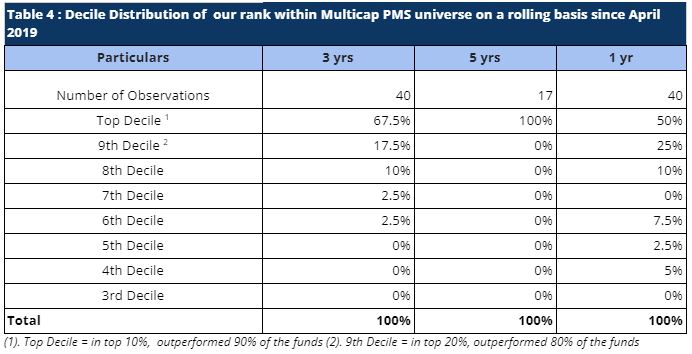

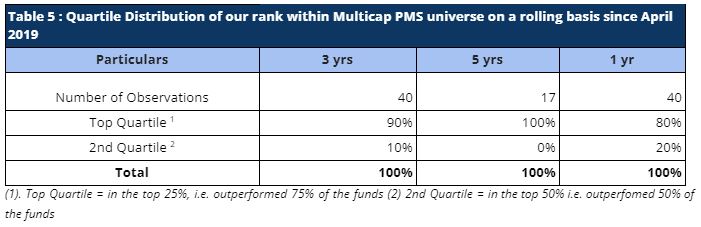

Rolling Returns and Rankings

Rolling returns are a more useful indicator of consistency in performance versus single period returns. For the rolling three year periods applicable for our entire operating history, we have been ranked among the multicap universe in the top decile 67.5% of the time (27 out of 40 observations) and in top Quartile 90% of the time (36 out of 40 observations). For the remaining 10% observations, we were ranked in the second quartile (Tables 4 and 5). Also, for the three year period, we have remained in top decile every single month on a consecutive basis for almost two years since July 2020. Similarly, for the rolling five year periods applicable for our entire operating history, we have been ranked among the multicap universe in the Top Decile 100% of the time (17 out of 17 observations)

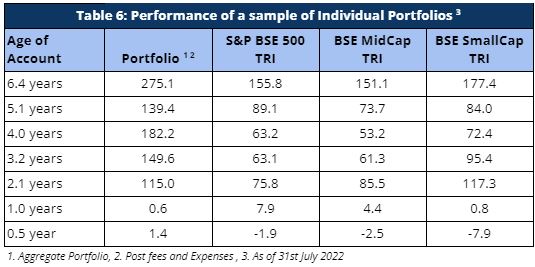

Performance Of Individual Portfolios

Portfolio returns for clients, except for investors starting with us over the last one year have seen remarkably strong alpha (Table 6). Performance of portfolios of clients who joined us in the last one year is a matter of concern that we hope to be able to address over time. We have discussed in detail about our average performance in the last one year in our annual investor letter.

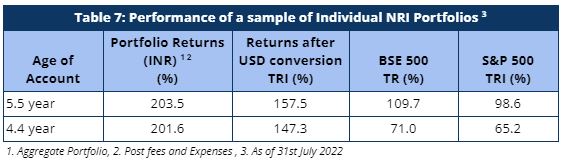

Our NRI clients have seen strong returns even after factoring in rupee depreciation against US dollars. The portfolio returns are significantly higher than both BSE 500 TRI and S&P 500 TRI, generating strong alpha over both these indices (Table 7).

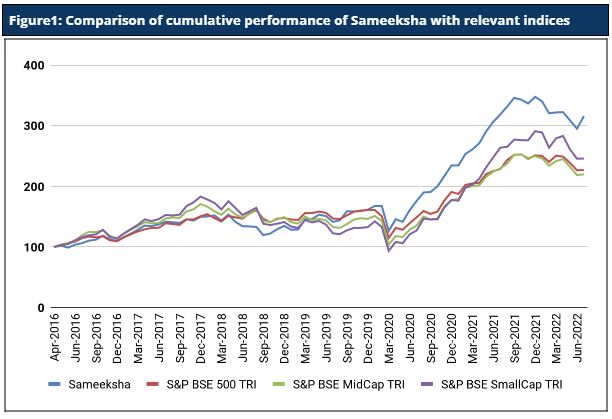

Cumulative Performance versus the benchmark

Sameeksha’s outperformance over its benchmark has continued to widen positively over the years. Even after factoring in the underperformance and the volatile market in the last one year, an investment of Rs. 100 with us since inception (April 2016) would have grown to Rs. 316, far outpacing what one would have earned by investing in a fund that achieved benchmark returns (Figure 1).

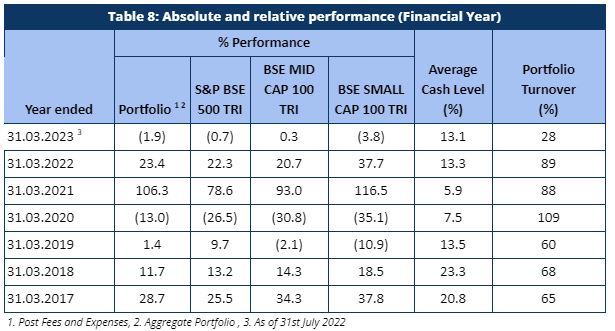

Fund Performance on a Financial Year and Calendar Year basis

For the first 4 months of the current financial year ending March 2023 (April 2022 to July 2022), Sameeksha PMS has marginally underperformed the benchmark BSE 500 TRI by generating -1.9% returns for the period against the benchmark -0.7% returns (Table 8).

Looking at our performance over the financial years, we have outperformed our benchmark in four out of seven financial years. Key however is that the sum of outperformance in those four years far exceeds the sum of underperformance in the remaining three years (including the current incomplete financial year).

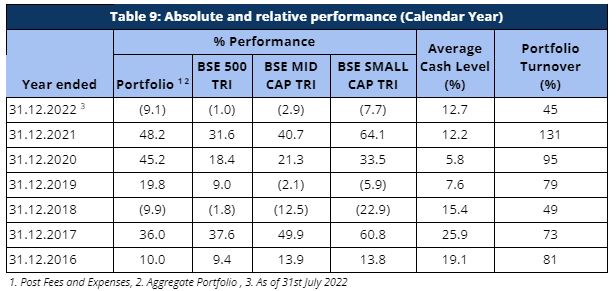

The performance pattern on a calendar year basis has been quite similar as well (Table 9). Although, for the current calendar year 2022, we are underperforming the benchmark, for the recently completed calendar year ending 2021, we have generated a return of 48.2% with an alpha of 16.6% over our benchmark BSE 500 TRI.

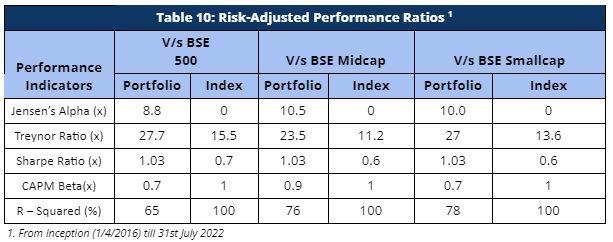

Risk Adjusted Ratios

When compared on a risk-adjusted basis (Table 10), our PMS shows even stronger performance with a risk-adjusted alpha generation of 8.8% over the broad market benchmark since its inception. While our portfolio beta has been materially lower than our benchmark, our returns have been higher than the benchmark since inception, implying superior strong risk adjusted returns.

Furthermore, other risk-adjusted returns – Sharpe ratio and Treynor ratio, are also significantly higher than the benchmark indices (Table 10). It is worth noting that we offer superior risk adjusted returns not only compared to the broad BSE 500 index heavily weighted towards large cap but also the small cap and mid cap benchmarks as demonstrated by our Sharpe ratio, Alpha, Treynor ratio and Beta.

Disclaimer : The information contained in this update is based on data provided by our fund accounting platform and is not audited